Stocks vs. Real Estate in Vancouver – November Webinar

Stocks vs. Real Estate

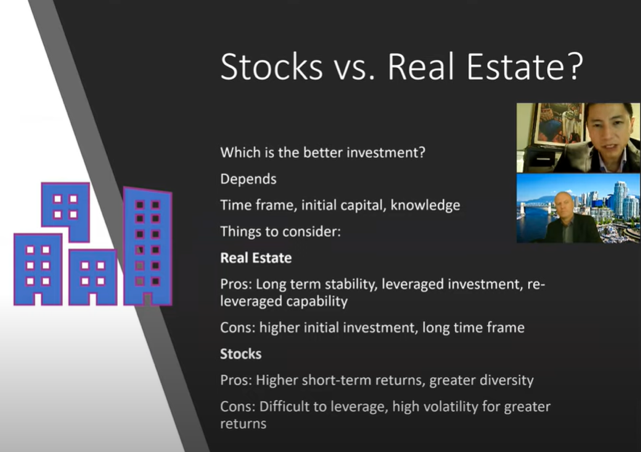

What are the pros and cons of stocks vs. real estate? Which is the better investment, and where should our money be?

It really depends on your time frame, initial capital (you need significantly more money to invest in real estate), and knowledge base (are you good at researching stocks or do you pass things over to an advisor? Do you come from a background of managing or researching good quality real estate?)

| REAL ESTATE | STOCKS | |

| PROS | Real estate has long term stability, can be leveraged (especially if you don’t have, say, $500,000 to put down on a property, as you’d need this up front for the same amount in stocks). With real estate the banks are willing to lend you this kind of money with 20% down on your own personal property, as little as 5% down. Because of this, you have a much higher capacity for an investment at a similar ROI. In real estate, you also have the ability to re-leverage capability. This means when your real estate is showing, say, $100,000-200,000 of equity, you can use that to purchase more real estate or stocks. You can’t do this with stocks—it’s very rare that a bank would allow you to borrow against your stocks without selling them. | In the short term, you can see some fantastic returns. For example, we were talking to clients about strategies to get into real estate when COVID hit in March and markets were down 27%. This included leverage strategies. Clients leveraged in $100,000 to the markets and are now up by 80%, though some are just up by 10-20%. You would very rarely get that in the real estate market in just 5-6 months. You also get better diversity capability with stocks over real estate. |

| CONS | High initial investment — with a 20% down payment, it will be in the tens of thousands of dollars, and you really need a long time frame horizon. If you need to liquidate your real estate in a year or two, you may not see any of the value you thought you’d get. | Stocks are difficult to leverage. If you wanted to use them to buy something else, you’d likely have to sell them, which means a taxable consequence. There is also a significant amount of volatility – you won’t get real estate going down to -32% one year and up to +54% the next. |

What is happening right now with Vancouver real estate?

COVID-19 is affecting everything. Starting in the 1980s until prior to COVID-19, people were going from lower density areas of the city, the suburbs, and moving into the core. This was a shift from about 1945-1985 of people going from the city out to the suburbs and low density places. Once COVID struck, everyone wanted to be away from other people—they don’t want to be stuck in elevators, hallways, or close proximity to people. People have been leaving condos in high density areas, like downtown or Metrotown, whether they’re renting or owning. The reason we know this is because of a concept called sales ratios. Say, for example, in a given month you have 100 listings in a market. Of these, you have 20 sales or a 20% sales ratio. We’re seeing much lower sales ratios in high density areas than we are in low density areas.

Areas and property types that are very busy include single-family houses in the suburbs, cabins, vacation properties, located further out from Vancouver, say, 45-90 minutes to get downtown. Maybe you have to take a ferry, but you can still get downtown. These are places like Victoria, Nanaimo, Squamish, the Fraser Valley, and Bowen Island. They’re very, very busy. At the high end of the market, single-family houses on the west side of Vancouver are very active.

Properties that aren’t doing so well include condos in the core of downtown Vancouver, and, to a lesser extent, Metrotown, Burquitlam town centre, and places like that with higher density where people need to share spaces like elevators, because they’re worried about COVID. Secondly, people are working from home and want more space to do so, especially couples. Two people working from home in 500 square-feet gets tight and tiresome very quickly.

These things are really changing the market, but I see opportunities in this situation. For example, some people looking to the future are getting some very good deals in downtown Vancouver. Rents across Canada, and especially in downtown Vancouver, are actually falling. As an investor, that might make you uncomfortable but it’s actually an opportunity because there are people in high density areas getting less rent who have had enough and want to sell, so you could get a very good deal on these properties. Rents have gone down for a few reasons:

- COVID has stopped immigrants from coming to Canada, and new people to the country usually start with a rental and very rarely buy.

- There are no foreign students coming here because of COVID.

- With travel restrictions due to COVID, there are little to no Airbnb rentals. People aren’t going to places like Tofino and Whistler. So, furnished rentals have hit the unfurnished rental market and these properties will likely go up for sale.

In a year or two, when we have a vaccine widely distributed, these properties will see a huge rebound in terms of rental rates, vacancies, and price surges once people realize COVID-19 is under control and they can live in high density areas. We all know why people live in high density areas: to walk to work, great restaurants and shopping, clubs and bars, and the seawall without having to get in your car and sit in traffic.

I concur. I’ve seen this type of thing before in real estate investing. People panic. Whatever situation we’re in, whether it’s the 2008 crash or the 2001 tech bubble, people think it will last forever. We’re already seeing signs of the vaccine coming. I’m completely ready to pull the trigger as soon as they say we can travel—I’m on a plane, with the kids in a hot destination at an Airbnb, VRBO or a hotel.

Seeing those discounts is one of the great things about working with someone like Mike who knows what’s going on for investment opportunities. Each month we do this webinar, it shifts and isn’t the same every time.

What’s pricing like right now? Are properties going for under-asking, over-asking, or as listed?

This goes back to sales ratios. In hot markets like North Vancouver, the west side of Vancouver, the Fraser Valley, Squamish, Victoria, and Nanaimo, properties are going for asking and sometimes above asking. The reason is we have ultra-low interest rates, with the Bank of Canada encouraging real estate investing. In these places with more space, where people can get more distance from one another, markets are doing fantastically well. Condos downtown and in high density places are challenged. The market isn’t dead, but it’s not as strong as low density areas. Overall, prices are and have been rising, and sales volumes are up about 29% from this time last year and are above the 10-year average, but this activity is from lower density areas.

For people that are waiting on the sidelines, what are the predictions for 2021?

Your crystal ball is as good as mine, but I think we’ll see a continued increase in property prices across Canada, and in Vancouver particularly, because the Bank of Canada and Federal Government use real estate as a way to reflate the economy. Right now, there’s talk of Canada being a 90% economy: 90% of people are working, and 10% are not. We can’t do all that we want and spend all that we want because of COVID restrictions. Once those restrictions go away, we’ll see the real estate market boom because there will be a lot more people wanting to come and stay here, by renting Airbnbs and unfurnished rentals. Also, the Bank of Canada has explicitly said they will keep the ultra-low interest rates for a significant period of time after the recovery has begun, which we’re just starting with. The low interest rates will make the cost of owning a property very low — you can get mortgages for under 2%, even as low as 1.6-1.7% on a five-year fixed, which is fantastic! If inflation goes past 2%, you’re getting paid to borrow that money.

You have tons of clients as investors, very wealthy people who invest in the stock market, so what’s your take on the pros and cons of real estate vs. the stock market?

I like that real estate is a tangible asset that will never go down to 0. With the stock market, we’ve seen scandals where a company we thought was great goes rotten and its value goes down to nothing. This doesn’t happen with real estate. Secondly, you can live in your real estate asset as it increases in value, which is lovely. Better to get the upside of capital appreciation than to pay someone else’s mortgage. What I really love about revenue properties and single-family houses with a suite is there are a lot of tax advantages, particularly for people who are self-employed or earn a high income. Check in with your accountant on this.

Yes. Except for the tax-free savings account, which is a small amount, any stock, mutual fund, or RRSP investment will eventually see a capital gains tax. But your own personal property is totally capital gains tax-free. This analysis is what my financial practice does for our clients. People still come to me saying they’ll rent and invest in the stock market because, come retirement, they’ll do better because of Vancouver’s high real estate prices. But that math is wrong — the capital gains savings, the leverage, and the amount of rent won’t put you ahead.

Return on Investment (ROI) is the annual interest rate of return compounded. All investments, including real estate and stocks, are measured by ROI.

If you look at the S&P 500, the 500 largest stocks in the US and the biggest stock market in the world, their ROI over the past 20-80 years has hovered from 8-10%. However, there are management fees and other factors, so a really good rate of return is a solid 8%. Some people get 12% and others are okay with 5%.

As an example, if I had $60,000 to invest, should I put it into a one-bedroom $300,000 condo or in a consistent 8% return stock? Both options are on a 25-year time frame. I would assume the condo appreciates at the same rate of return over the 25 years and that I’m starting with a 3% loan rate (which the very low rates we have now could easily increase to). I would also have a renter who would pay off a portion or the entire mortgage. A good advisor can calculate the vacancy and any fees.

I’m using a financial calculator, which you can download.

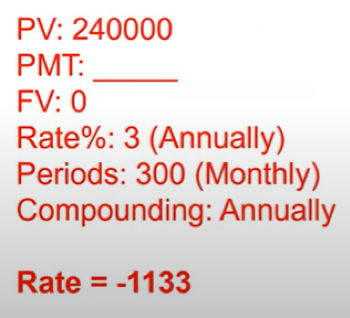

For the condo:

- Present value (mortgage)= $240,000 after putting $60,000 down on the $300,000 condo

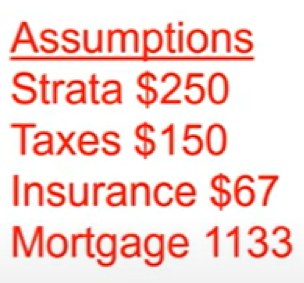

- Monthly payment is about $1,600 per month ($1,133 per month to own the condo plus assumptions of extra fees)

- You might be getting $1,400 in rent, plus maybe a vacancy period and property management fees

I tell clients not to get a property with too great of a shortfall in terms of monthly subsidy for the property. A small one is alright because rent goes up and mortgage goes down, which means in, say, five years, that shortfall of the subsidy is covered.

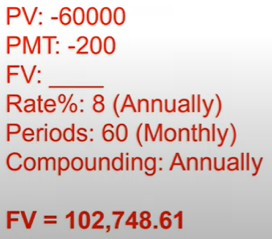

For the $60,000 stock:

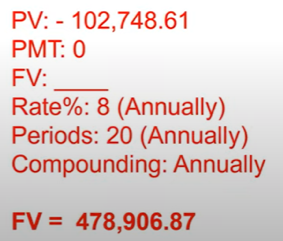

In order to match the condo comparison, I need to contribute $200 a month for five years. After five years, I’ll have $102,748.61. For the next 20 years, there’s no more $200 deposit and I don’t owe more money, so I’ll have a little under $500,000. This is on the best day, as it’s a consistent 8% over 20 years.

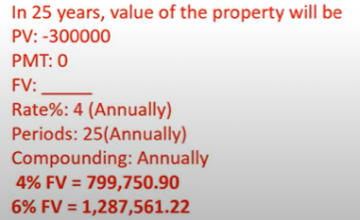

What is the value of the condo at this time, and how does that compare to the $478,907? History has shown that a Vancouver condo will probably be around a 4% (ROI) growth rate, while a house with land is about 6%. This brings it to about $800,000 in 25 years at 4%, or $1.288 million in 25 years at 6%.

The stock was at $479,000. Even if I brought the number down further, the condo would win out for other reasons:

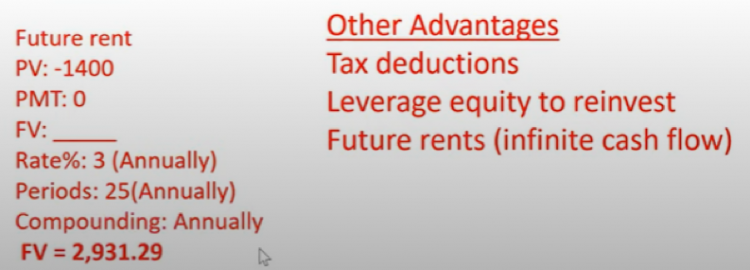

- Tax deductions: you can deduct the mortgage interest, strata fees, property taxes, and any form of vacancy

- You can leverage it to reinvest — say after five years you have $80,000 of equity, you can pull that out and reinvest it in other real estate or the stock market

- Future rents are infinite cash flow unlike stock (you could get a dividend but it wouldn’t be as high as rents) – in the first year, rent was $1,400 and, based on past analysis I’ve done, we can assume about a 3% per year increase on average (this is market rent for a new tenant, not year to year with the same tenant, as the government dictates how much you can increase rent by in that case).

I’d get $2,900 per month in 25 years for a fully paid off piece of real estate, and this will keep growing year after year!

I own multiple pieces of real estate for this reason. Especially for people who are self employed, this is your own self-funded pension.

These are some reasons why I love real estate, but don’t get me wrong — I also like the stock market, and in 2020, we had a fantastic opportunity there that many of my clients and I took advantage of.

The philosophy at Latitude West has always been a mixture of stocks, real estate, and a form of reserve (for instance, the equity within real estate itself). I invite those that love real estate and have some money in the markets, but don’t have a financial advisor combining these together to contact me.

Don’t try to time or predict the market – instead, create a strategy that will work in any market. I review the strategy with clients to see if it makes sense. I always like a long-term horizon, which is probably why I like real estate so much.

At Latitude West, you can book a Discovery meeting which doesn’t cost anything and is just about us getting to know each other.

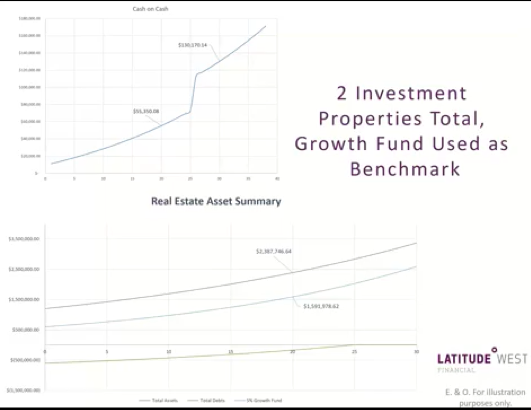

We assess multiple real estate properties to see how many properties make sense — one, two, leverage off the first, or even get a third down the road.

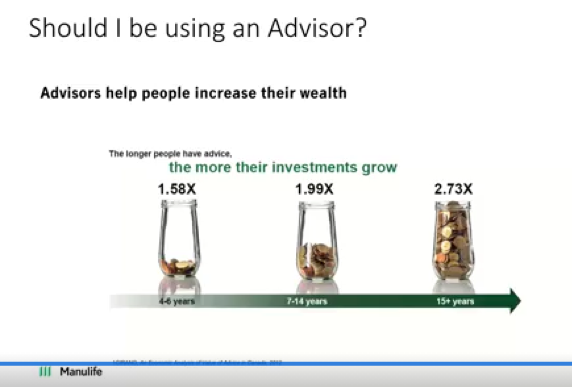

Manulife Financial found that when you use an advisor, your wealth multiplies compared to when you don’t. This isn’t because you can beat the markets, but because the advice and strategy is about things you may not have otherwise known about. This isn’t just financial advice, but real estate, too. Someone like Mike can help to see if you should be buying multiple properties or, say, upgrading your condo to a house or keeping a tighter cash flow and owning both.

Questions

What is the best percent allocation of stocks, real estate, and reserves?

It really depends on what stage of life you’re at. But, the wealthiest investors in the world are part of a group called the Tiger 21. Every year, there’s a study on them, as everyone wants to know where their money is. It’s found that 40% of their net worth is either in the stock market or their own business, 38% is in real estate, and the remaining 22% is in reserve. I personally have a lot of my wealth in real estate, so I am a bit biased, but my knowledge base of real estate is very high, as is Mike’s. So, for the average person, I would not put the majority of their wealth in any sector they’re unfamiliar with. As your knowledge increases in any sector, you should put more into it and your earnings increase, too.

When my kids hit their twenties, my advice will be to start with the stock market until they can afford a down payment, then put that into real estate. Then, grow the real estate, pull the equity out as soon as they can, likely in 4-5 years, to reinvest in more real estate. However, if the stock market is down or crashes — which is rare, like once every ten years — take some short-term 1-2 year gains off of the leverage. The deal of a century happens once in a lifetime, and you only lose money when you sell, so try to hang on during a crash.

If the stock market is down 20% ROI from its peak, you have a sale. If it’s 30%, you have the sale of a generation! Historically, if this happens, on average, it will take 1-2 years to get back to its original location which means a 30% gain within one year at that point. That’s why I say all investors should understand all of the pieces and take advantage whether it’s a sale on the stock market or real estate.

So, everyone is different but you’re doing yourself a disservice if all of your money is tied up in one sector and not the other.

As an investor, is it better to purchase property as an individual or through a holding company?

Although there are significant advantages to buying through a holding company for the right circumstances and businesses, I would definitely talk to your accountant and financial planner to determine how to best structure it. They know your financial situation best, so work with them and your mortgage broker on this. Christian or I can recommend an accountant if you need one.

I echo that. I wouldn’t buy real estate through a holding company without getting professional advice—it’s dangerous advice to follow just from a recommendation. Even accountants don’t do what financial advisors do with cost-benefit analyses to see, mathematically, what makes the most sense. As a quick example, if you’re incorporated and can quickly move money from an operating to a holding company, you have a lot of retained earnings, and you’re in a very high tax bracket, a holding company will probably make sense, especially if the place is cash flowing. But this is very rough and I’d need to look at your situation more closely.

People are working from home now, but in the future do we expect more people to come back downtown? Where is the better investment for the future, downtown or the suburbs?

I’ve been thinking a lot about this and believe people will come back to the office, but certain people will still work from home. The COVID-19 pandemic has proved to more senior, older, or mainstream-minded people in organizations that it is possible and effective for people to work from home, but the office and working together in close proximity has distinct business advantages. Once we have a vaccine, I think a lot more people will be coming back to the office. We won’t see the end of the office, but we will see certain businesses and more people still working from home.

In terms of opportunities, I see the core as a really good one right now, along with other places that were really busy before COVID-19 and aren’t now. Things will change back to normal, though maybe not 100%, once we have a vaccine. A lot of things not happening now will happen then, and the core of the city is somewhere you should look. I think the suburbs are expensive now and will soften when a vaccine comes.

I remember in 2008 a lot of clients thought there was opportunity in the stock and real estate markets and wanted to know which direction to take. In 2008, it didn’t matter what piece of real estate you bought in all of the Lower Mainland or the Fraser Valley—10 years later, it all went up! So, now, if you have a 10-year time frame, the answer is you’ll make money.

My concern as a financial advisor is what the cash flow will look like in the short term—will you be -$1,000 because you bought a place you didn’t know how to assess? Will you be over-leveraged to death and living off of mac & cheese? I care more about whether you can afford what you’re planning to buy, if it has good appreciation, and if the vacancy will be low. You can’t go wrong with real estate.

But when you’re looking at a revenue property, you’ve got to buy it right. Cheap, simple, and high quality. You don’t want fancy, beautiful, or what blows someone away. You want one of many, so if it breaks, it’s easy and cheap to fix and doesn’t break your heart.

What is your opinion on investing in real estate vs. a REIT (real estate investment trust)?

A REIT is another category of a stock. There’s healthcare, there’s consumer staples, and others, and REITS is one of them. You own a piece of different real estate properties and get an ROI from it all. It’s basically saying you want to invest in the stock market and is very different from what we’re talking about today. It’s a diversification of your portfolio and if you want exposure to all of the advantages we’ve talked about — like rental cash flow, capital appreciation, or tax deductions — then you’re not doing REITs.

But, you also need to consider your lifestyle when making this decision. Everyone is different. Are you super busy? Do you have time to deal with tenants? These are not one-size-fits-all pieces of advice, and you’ll want to talk to an accountant, financial planner, mortgage broker, and realtor to get a customized solution for your personal retirement plans, investment plans, and so forth.

Is the North Shore a good investment at the moment?

The North Shore is good. I like it and live on it, and I think there are some good presale condo opportunities there. Some projects in Lynn Valley and elsewhere pre-sold and are worth less than what people originally paid, so there are sellers you can do really well with by buying on assignment. It’s such a big area and there are so many types of properties.

I also live on the North Shore and my property values have gone up quite a bit since I moved. I was looking at other areas but noticed the North Shore tends to always hold its value. If the real estate market takes a hit, the North Shore will maintain or won’t get hit as hard. Plus, when things go up, the North Shore tends to be about 1-2 points above everywhere else. It’s a great place to live, but for investment purposes, again, I would get a good financial advisor to do an analysis of a cross-section: North Shore, Burnaby, Chilliwack, etc. Sometimes the best deals are in places which you would never live, but that doesn’t matter if it’s just an investment.

Case in point: in the Fraser Valley, you’ll get cap rates and capital appreciation that is far higher than anywhere west of Surrey. The key to look at with all of this stuff is what your personal goal is (e.g. capital appreciation, revenue, tax efficiency, etc.), what age and stage of life you’re at (as you get closer to retirement, you’ll want more certainty and cash flow, but younger people don’t necessarily need that). Talk to the professionals we mentioned and come up with a solution that works best for you to help reach your financial goals—that’s what this is all about.